Facility Association insurance? There’s a good chance that you’ve never heard of this organization or the insurance services it provides.

And if that’s the case, good for you!

But for many Canadians, there are times when typical car insurance just doesn’t cut it. It can be for a variety of reasons – and quite often, they’re not great reasons. This is where the Facility Association enters the picture, providing auto insurance for those who likely need it the most.

Here, we take a look at what Facility Association is, who and how it can help, and where in Canada you have access to its services.

Let’s get started.

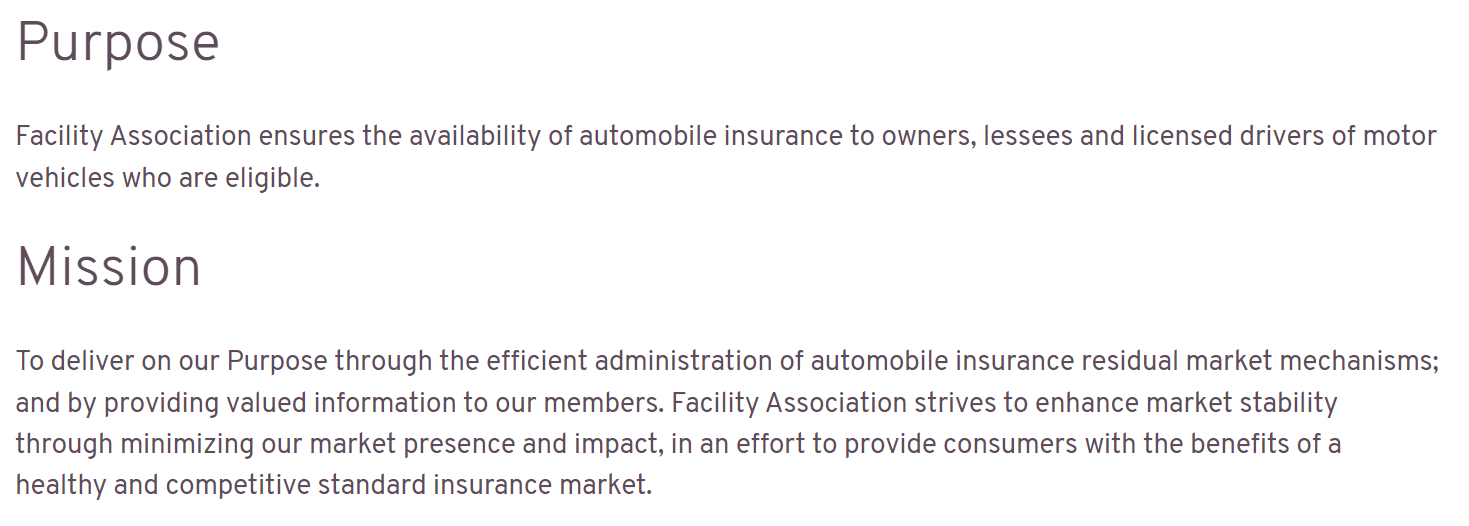

Facility Association – who or what is it?

At first, it might sound like an organization that provides venues for various events, but the Facility Association is actually an association of Canadian auto insurers.

Yes, there are probably dozens of insurance associations across the country, but this one has a unique and specific purpose: to make sure all Canadians have access to car insurance, no matter the risk.

Here’s the association’s mission statement:

To put it in more simple terms, this association guarantees that every licensed insurer in its jurisdiction is able to offer auto insurance even to people who would normally be considered high-risk clients.

This allows everyone to be insured, so there are less accidents involving uninsured motorists, which cuts down on risks for all of us.

Who can benefit from Facility Association insurance

Unfortunately, there are many reasons why Canadian drivers might be forced to accept alternative car insurance.

You may need Facility Association insurance options if you have the following:

- no driving experience,

- a poor driving record,

- a vehicle that’s considered high risk,

- an extensive history of prior insurance claims,

- a history of using your vehicle in unsafe ways, or

- past payment inconsistencies and/or problems.

Another that will affect your insurance eligibility is if you’ve committed any type of insurance fraud in the past.

Essentially, we all benefit from what the Facility Association provides. Their work keeps the market stable and effectively ensures that typical, safe drivers have access to reasonable premiums.

A note for those with bad payment histories

If you’ve had issues with paying your bills on time in the past, there are tools and tricks that can offer some help. For instance, there are loans and credit cards for bad credit as well as debt consolidation options.

Taking advantage of these opportunities might give you the help you need to set things straight, and you’ll hopefully be eligible for typical car insurance premiums once again.

How is this different from other forms of insurance?

We know how typical insurance works, but the type of insurance provided through the Facility Association insurers is a bit different.

Here are a few details that set these policies apart.

They’re only available to those who can’t get insured elsewhere

This type of insurance is a last resort.

When you don’t qualify for the policies that average drivers are typically offered by insurance providers, you’ll be presented with an alternative insurance plan. This is where the Facility Association can help.

It’ll cost significantly more

Those who have this type of insurance are likely paying 2 to 3 times more than the average driver. This is simply because of the risk involved with insuring these individuals and potentially unsafe vehicles.

For instance, if you’re a driver who’s been in multiple car accidents over the last 5 years, it’s statistically likely that you’ll be in more accidents, and this means your insurance company will have to pay out again.

The high risk level the company takes by insuring you is mirrored by the high prices.

They’re purchased through a different type of market

Average car insurance is purchased through the “voluntary market,” which means the insurance companies voluntarily compete for your business.

Facility Association-type insurance, though, is bought through the “facility association residual market” or FARM. It’s simply a different market specifically for vehicle owner and operators who need insurance but have trouble getting it.

Facility Association insurance availability

You might be surprised to learn that the Facility Association doesn’t operate in every province or territory within Canada.

Let’s look at where it does operate, where it doesn’t, and why it isn’t nationwide.

Where you can get Facility Association insurance

To start, here are the provinces and territories where Facility Association insurance is available:

- Alberta,

- New Brunswick,

- Newfoundland and Labrador,

- Northwest Territories,

- Nova Scotia,

- Nunavut,

- Ontario,

- Prince Edward Island, and

- Yukon.

If you’re having trouble finding typical auto insurance through the usual means and you live in one of these provinces or territories, you’ll be eligible for a Facility Association policy.

Where you can’t get it

And here are the provinces where Facility Association doesn’t operate:

- British Columbia,

- Manitoba,

- Saskatchewan, and

- Quebec.

The reason why Facility Association doesn’t operate in these areas is simply because there are other governing bodies and regulations in place that accomplish the same goals.

And, actually, these provinces receive car insurance through the provincial government, so it’s the government that’s regulating things.

You may not always need Facility Association insurance

If you do find yourself in the unfortunate position of having to pay for a Facility Association insurance policy, don’t get too downhearted – it doesn’t have to be forever.

As long as you work hard to keep a clean driving record, you should eventually have a chance to break away from your pricey insurance plan.

After a few consecutive years of a clean record (one that’s free of accidents, tickets, etc.), you’ll once again be eligible for a less complicated policy from a typical insurance company.

And you’ll hopefully be able to save money by switching.

What are your thoughts on Facility Association insurance?

While it’s rare that drivers have to go through the Facility Association to get proper insurance, it certainly does happen. And this makes Canadian roads safer and Canadian drivers more confident.

Are you familiar with Facility Association insurance? Do you have or have you had one of their policies? How did it work out for you?

We love hearing about our readers’ experiences, so feel free to leave your thoughts in the comment section below.

FAQ

What is Facility Association insurance?

Facility Association insurance is auto insurance for certain drivers who aren’t able to obtain typical insurance from private companies. This could be due to a poor driving record or a number of other factors. You can read here for more info about how this insurance is different from typical policies.

Why are the Facility Association rates so high?

Unfortunately, policies through the Facility Association are much higher than typical plans. This is simply because of the risks associated with offering coverage for these individuals and vehicles. If your insurance company feels it’s likely it’ll have to pay out when you get into another accident, they’re going to charge you more on a monthly basis.

Is the Facility Association for profit?

Actually, no, the Facility Association is a non-profit organization. It’s simply an association that ensures private insurance companies can and do offer policies for high-risk drivers and their vehicles. You’ll find more information about the Facility Association here.

How can I get Facility Association auto insurance?

You can get this type of insurance through any insurance agent located in an area where Facility Association operates – you’ll find these areas listed here. Other areas of Canada have different governing bodies overseeing car insurance matters, so Facility Association insurance isn’t an option there.

Leave a comment

Comments